For years, we’ve heard about a battle between payment methods cards, digital wallets, bank transfers. But I believe this misses a deeper, quieter shift. It’s not about how you pay at the checkout.

It’s about where your money lives before you even get there.

Your Money in Walled Gardens

Most of us are used to open-loop money: your debit card, credit card, or bank account. These work almost anywhere.

But there’s another kind: closed-loop money. This is value that lives inside a specific app or store.

Think:

Your Amazon gift card balance

Starbucks rewards stars

Uber Cash

Store credit from a return

Credits in a gaming app

This isn’t new. What is new is how big and strategic these “walled gardens” have become. Companies are designing experiences so you keep money inside their world.

Why Companies Love “Stored Value”

From a business perspective, it makes sense. If you already have a balance in their app, you’re more likely to return. It costs them less in fees, and they learn more about your habits.

For you, it can mean more perks, smoother checkouts, and tailored rewards.

The Unseen Consequence

Here’s what often goes unnoticed: when you pay with a gift card balance or loyalty points, no “traditional” payment happens. Your credit card network doesn’t see that transaction, even though a sale occurred.

The real competition is shifting—from the moment you tap your phone, to the moment you load money into an app.

The Path Forward: Connection, Not Just Competition

This isn’t a winner-takes-all fight. The future isn’t closed-loop or open-loop—it’s both.

The opportunity lies in connecting these systems. Imagine seamlessly using rewards points across different stores, or moving value between apps as easily as sending a text. The infrastructure behind your credit card is perfect for enabling this.

What This Means for Us

The next decade in payments will be defined by how these two models work together. The businesses that succeed will be those that blend the convenience of stored value with the flexibility of your traditional cards.

They’ll design experiences that feel simple for you, while being smart about where your money resides.

That’s the real shift happening right under our fingertips. It’s not just about how you pay. It’s about where your money calls home.

Lately, I’ve been following the news around Trump’s recent announcements on tariffs. He’s paused new tariffs for 90 days for most countries but increased them significantly for imports from China. A lot of people are quick to call this move “bad for the economy” or “protectionist.” But as someone without any background in economics—just a curious mind—I wanted to unpack this a little differently.

What if, instead of seeing this as a power play, we look at it as the U.S. trying to even out the trade rules?

Think about it this way: if you’re running a food stall and every time you export your burgers to another market, they charge you a fee, but when they send their noodles to your market, they don’t pay anything—over time, that adds up. You’re playing a game where the rules aren’t the same for both players. So, when the U.S. matches the tariff rates that other countries already impose on American goods, can we really call that unfair?

That doesn’t automatically make it good policy—but maybe it’s not about being “bad,” either.

Let’s look at a real-world example. Europe charges higher tariffs on certain U.S. agricultural products. China has long had stiff import duties on American cars and tech products. If the U.S. raises tariffs to match those levels, is it protectionism or just self-defense?

But here’s where it gets interesting: instead of getting stuck in a tit-for-tat tariff spiral, maybe we should step back and ask—what kind of global trade do we actually want?

Do we want a race to see who can out-tariff whom, or do we want trade that’s based on actual value and mutual need?

Imagine a world where countries trade based on what’s most useful for their people, and where the goal is win-win—not win-lose. Like, say a Southeast Asian country has a surplus of rice and needs solar panels. Meanwhile, a Western country has excess solar tech but imports most of its food. That’s a trade based on value and need—not politics or power.

It’s kind of like swapping toys as kids—one of us has a remote-control car, the other a LEGO set. We trade, not because someone “wins,” but because both of us get something we genuinely want.

So maybe this is a good time to reimagine global trade. What if instead of calling tariffs “good” or “bad,” we started asking better questions?

Does this policy help both sides in the long run?

Are we encouraging trade that supports local industries and opens up access to needed resources?

Can we redesign agreements to be flexible and collaborative, instead of punitive?

I’m still learning, but one thing seems clear: trade doesn’t have to be a battlefield. It can be a bridge—if we let it.

Over the past few years, I’ve spent a lot of time working in the payments space across Asia. One thing that consistently fascinates me is how consumer financing tools, especially instalments, have evolved — and how different models are starting to intersect. This piece is simply a reflection of what I’ve observed, what I think could be possible, and what I’m still trying to learn more about.

Cards vs BNPL: Same Need, Different Paths

Before BNPL became a buzzword, many of us were already familiar with card-based instalment plans. You’d swipe your card at an electronics store or during a holiday booking, and the bank would let you pay it off over 3, 6, or 12 months. These were real credit products — backed by regulated institutions with clear terms.

BNPL came in with a fresh approach — simpler UX, fast approvals, and merchant-led integrations. It made sense, especially for digitally native users and smaller ticket sizes. But as the BNPL model has grown, so have questions around credit risk, regulation, and sustainability.

From what I’ve seen, card-based instalments offer a more robust framework — one that’s credit-scored, pre-approved, and tied into a broader financial ecosystem. But they often fall short on ease of use and visibility at checkout. There’s a clear gap, and perhaps a huge opportunity, in marrying the reliability of cards with the simplicity of BNPL.

Why Cross-Border Instalments Matter

One area I believe is deeply under-explored is enabling card instalments for cross-border spend.

Intra-Asia travel is growing. Shoppers from Malaysia are buying in Japan, Indonesian tourists are visiting Singapore, and online platforms now cater to customers from multiple countries. And yet, if I use my local card overseas, there’s rarely an option to convert that transaction into an instalment. Why not?

If we can enable real-time, cross-border instalment options — say, a Thai cardholder buying a handbag in Seoul or booking a stay in Bali — we could unlock incremental business for both merchants and issuers. Consumers get flexibility and affordability. Merchants close more high-value purchases. And banks retain spend on their cards instead of losing it to local BNPL or deferred wallet payments.

The infrastructure exists. It’s just a matter of connecting the dots — acquirer readiness, issuer cooperation, and smart UX at checkout.

The Role of Wallets & Local Payment Schemes

Wallets and local A2A payment schemes (like UPI in India, DuitNow in Malaysia, QRIS in Indonesia) are becoming the default rails for everyday payments. They’re convenient, widely accepted, and increasingly trusted even for higher-value transactions.

This shift makes me wonder: can we bring the concept of instalments into these flows?

Many wallets already offer “Pay Later” features, but it’s usually in isolation. What if wallets could partner with banks or financing entities to offer instalment plans — backed by real credit limits, accessible at checkout, and even tied to dynamic offers?

For example, imagine booking a family vacation using your wallet, and being shown three instalment options — funded by your bank, or by the wallet itself if you’re eligible. It’s simple, integrated, and inclusive. We’d be meeting consumers where they already are.

Adding Loyalty to the Mix

Another angle I’ve been exploring is how loyalty can play a role in making instalments more attractive.

What if, instead of just offering “0% EMI,” we layered in accelerated rewards — 2x points for using instalments on a travel site, or a cashback voucher if you choose a 6-month plan at your favourite store?

This not only drives usage but also brings merchants into the equation. It becomes a value-added service, not just a financing tool. Loyalty, when linked smartly to instalments, can influence behaviour — and help both issuers and merchants deepen engagement.

Can Stablecoins Play a Role Too?

I’ve also been thinking about whether stablecoins — especially fiat-backed ones — could enable instalment flows, particularly in cross-border use cases. They’re fast, transparent, and increasingly being explored by wallets and fintechs across Asia. If regulated well, stablecoin-based instalments could simplify FX, reduce costs, and open up new credit rails that work across borders and ecosystems. I’m still learning here, but it’s definitely a space worth watching.

Making It Inclusive: A Broader Purpose

Perhaps the most important question I’ve been asking myself is — can instalment models be used to improve access for those who need it most?

There are still many in our societies who struggle to pay for essentials — education, healthcare, even energy bills — in one go. Instalments, if done responsibly, could make these expenses more manageable.

What if governments or public sector banks could partner with wallets or card networks to offer subsidized instalment schemes for select categories — with lower or no interest, for pre-qualified users?

It wouldn’t just be a product. It would be a policy tool. And it could genuinely help uplift the most vulnerable segments of our economies.

Conclude:

These thoughts are still evolving. I’m not claiming to have all the answers, but what I do know is this: the idea of instalments is being redefined in Asia.

It’s no longer about just cards or just BNPL. It’s about creating ecosystems where cards, wallets, QR payments, rewards, and even government programs can come together to offer smarter, fairer ways to pay.

I’m still learning — and always open to hearing from others who are thinking about these challenges too. If this resonates with you, let’s connect.

Rising stress levels and unhealthy lifestyles are leading to a surge in critical illnesses among young adults in their mid-30s to early 40s. According to the WHO, non-communicable diseases (NCDs) account for 74% of global deaths, and access to life-saving treatments remains a challenge. Some essential drugs can cost $2,000 to $40,000 per dose, making them unaffordable for many middle-class families.

Having personally witnessed this struggle, I’ve been working with leading pharmaceutical companies to explore fintech-driven solutions that make healthcare more accessible. The pharma industry operates within a highly regulated ecosystem of doctors, clinics, and pharmacies, but fintech can bridge critical gaps in affordability and accessibility.

How Fintech Can Transform Pharma

✅ Automation – Fintech enables digital distribution networks, increasing visibility and efficiency while reducing costs. A McKinsey report states automation can cut healthcare administrative expenses by 30%. ✅ Awareness – Digital patient enrolment programs can educate patients and provide real-time data on drug efficacy. QR codes at hospitals and pharmacies can drive awareness and facilitate quick enrolment. ✅ Affordability – A mix of stored-value wallets, automated discounts, and instalment plans via credit cards or NBFIs can ease financial burdens. In low-income countries, 40% of healthcare expenses are paid out of pocket (World Bank). ✅ Accountability – Government-linked grants can be directly credited to digital wallets, ensuring funds reach the right patients and eliminating middlemen. ✅ Growth for Pharma – Companies that adopt fintech solutions can expand their market reach and revenue while improving patient access. Digital transformation in pharma could add $200B in revenue by 2030 (PwC).

The Future of Fintech in Healthcare

The fusion of fintech and healthcare presents a game-changing opportunity to reduce financial barriers to life-saving treatments.

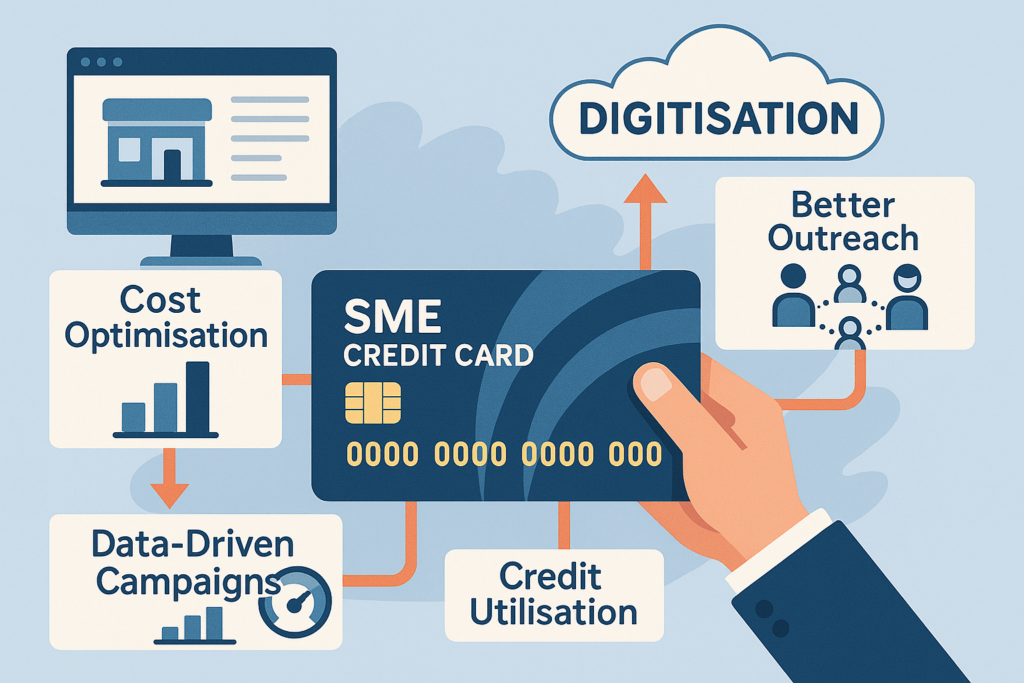

SMEs power 40%+ of Southeast Asia’s GDP—yet they’re still stuck between two worlds:

✅ The opportunity: Digital payments are exploding (e-commerce, ads, logistics, B2B flows). ❌ The roadblock: Rising fraud, fragmented tools, and a lack of scalable credit.

For banks, this isn’t just a gap—it’s a $100B+ opportunity waiting to be unlocked.

But here’s the catch: SMEs don’t need another “feature-rich” card. They need smart, secure financial tools built for their real-world problems.

🔐 Digital Growth ≠ Digital Risk

Every new payment channel (suppliers, ads, logistics) is a fraud vulnerability. One chargeback can shatter an SME’s trust in digital payments.

Banks hesitate: “Will SME cards increase our fraud exposure?”

The answer? Not if you layer the right defenses: ✔ AI-powered, real-time fraud monitoring ✔ Dynamic spend controls (merchant-specific limits, velocity rules) ✔ Virtual cards + tokenization to minimize exposure

The goal? Enterprise-grade security for businesses of all sizes.

🚀 Stop Selling Cards. Start Solving Problems.

The best SME programs don’t lead with “here’s a shiny new product.” They embed payments where they matter most: → Supplier payments (no more manual reconciliation) → Marketing & ads (controlled budgets, instant approvals) → Employee expenses (automated tracking, no more spreadsheets)

Winning formula? Fewer vanity features, more frictionless flows.

🤝 Why Banks Can Move Faster Than Ever

Mastercard, Visa, and fintechs have already built the rails: 🔹 Mastercard Biz360 – Digital tools for SME efficiency + security 🔹 Visa Commercial Pay – Virtual cards + spend controls for B2B 🔹 Fintech partnerships – Faster onboarding, alternative underwriting

The pitch to banks shouldn’t be:“Let’s launch a card.” It should be:“Let’s solve working capital, fraud, and cash flow headaches—with zero added risk.”

💡 The Bigger Vision

This isn’t just about payments. It’s about: ✔ Driving financial inclusion for SMEs ✔ Growing commercial spend volumes safely ✔ Becoming a long-term partner—not just a lender

The tools are ready. The demand is there. The question is: Which banks will lead the shift?

Thoughts? How else can banks build SME programs that actually move the needle? Let’s discuss.

Just sharing some personal reflections here.This thought actually came from a LinkedIn post I read last week, and it sparked a bit of a deep dive on my end. Tokenisation is something I’ve been trying to understand better — what I’m sharing here is a mix of my own learning, research, and thoughts. I’m not an expert, just someone curious and trying to connect the dots.

In Asia’s fast-moving digital economy, consumers juggle multiple cards, apps, and logins—banking, transit, loyalty programs, and government services. But what if a single universal token, secured by AI, could replace them all? From India’s Aadhaar to Singapore’s Smart Nation, Asia is already pioneering this future.

The Vision: One Token for Everything

A universal token would act as a digital passport for all transactions:

Payments: Replace credit/debit cards with a tokenized wallet (e.g., Alipay, PayNow).

Transit: Use your phone or wearable for metro, buses, and tolls (like Hong Kong’s Octopus Card).

Loyalty & Retail: Earn and redeem points seamlessly across brands (e.g., Rakuten Super Points).

Government ID & Services: Access healthcare, voting, and subsidies with a single login (India’s Aadhaar, Thailand’s Digital ID).

Grants & Welfare: AI-verified tokens could reduce fraud in social disbursements (e.g., India’s DBT).

Asia’s Leading Examples

1. Digital Identity: The Foundation

India’s Aadhaar (1.3B+ users) enables biometric authentication for banking, SIM cards, and welfare.

Singapore’s Singpass lets citizens access 1,400+ services—from taxes to private banking—with one login.

Thailand’s National Digital ID plans to integrate with banking and e-government services by 2025.

2. Payments & Transit: Tokens in Action

Hong Kong’s Octopus Card—one of the world’s first universal smart cards—works for transit, retail, and even school attendance. Now expanding to mobile wallets.

China’s Digital Yuan (e-CNY) tests programmable money for subsidies, smart contracts, and cross-border trade.

Japan’s Suica & Mobile Wallets (Apple Pay, Google Pay) allow seamless train rides and payments via smartphones.

3. AI & Security: Making It Trustworthy

Ant Group’s AI-powered fraud detection analyzes billions of Alipay transactions in real-time.

Singapore’s MyInfo uses AI-driven KYC (Know Your Customer) to auto-fill forms securely.

4. Cross-Industry Loyalty & Beyond

Rakuten Super Points (Japan): A universal loyalty currency accepted across e-commerce, travel, and brick-and-mortar stores.

Starbucks Odyssey (Singapore, Japan): NFT-based rewards program allowing tokenized memberships.

South Korea’s Zero Pay: Government-backed QR payments with integrated merchant discounts.

Challenges & the Road Ahead

While Asia leads in adoption, hurdles remain:

Privacy vs. Convenience: Balancing Aadhaar-like scale with GDPR-style protections.

Interoperability: Can India’s UPI, Singapore’s PayNow, and China’s e-CNY work together?

AI Governance: Preventing bias in biometrics (e.g., facial recognition errors) and ensuring ethical AI.

The Future: A Unified Asian Digital Ecosystem?

The pieces are in place—digital identity, tokenized payments, AI-driven security, and cross-industry loyalty. The next step? A pan-Asian framework where a Malaysian tourist can use their home e-wallet in Tokyo’s subway, redeem loyalty points in Bangkok, and verify their ID for a hotel check-in—all with one token.

Call to Action:

Which Asian country do you think will fully achieve this first?

Would you trust an AI-managed universal token?

Let’s discuss in the comments! #DigitalIdentity #AI #Fintech #SmartCities#banks#mastercard#Visa#Stripe#paypal

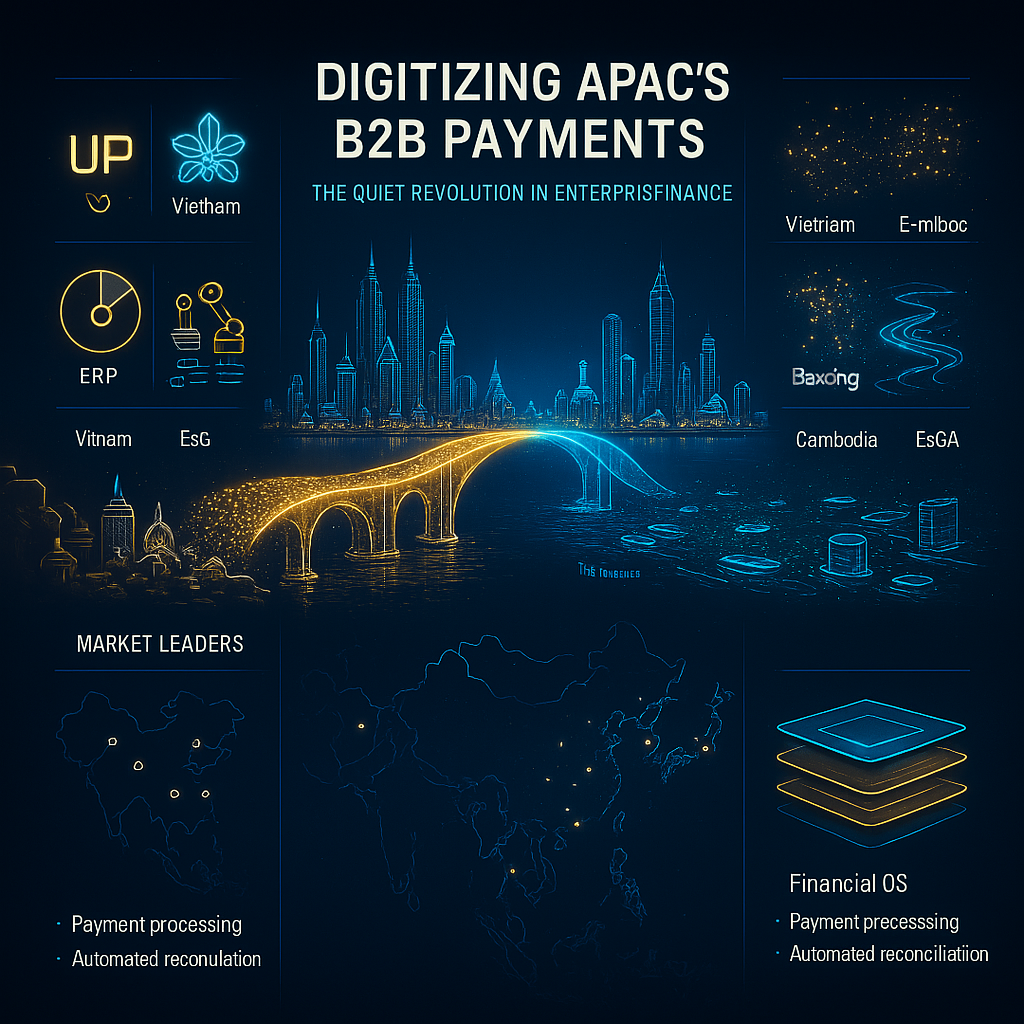

The payments space in APAC is undergoing a quiet revolution. While consumer payments have grabbed most of the headlines over the past decade, an even larger opportunity is emerging in the background: the digitization of over $50T in B2B payment flows across the region.

As someone keen to keep learning about evolving payment trends, I’ve been exploring this space more deeply—and it’s clear that the transformation of enterprise payments in APAC could unlock massive value.

What’s Driving the Shift?

Here are three drivers I found particularly compelling:

🔹 Regulatory Momentum Progressive policy moves are laying the foundation for digital B2B payment ecosystems:

India: UPI infrastructure now processing over $8T in annual B2B flows

Singapore: Project Orchid advancing CBDC use cases for cross-border trade

Australia: Nationwide e-invoicing mandates projected to digitize $130B+ in transactions

🔹 Enterprise Demand for Efficiency Businesses across APAC are actively looking to improve payment processes:

78% of CFOs cite payment automation as a top priority (McKinsey, 2023)

Commercial card penetration is still <10% in most markets

Estimated $4–6T in card-addressable B2B flows remains untapped

🔹 Emerging Market Momentum Smaller markets are moving quickly and creatively:

Vietnam: SME sector growing at 15% CAGR with over 500K businesses adopting digital payments

Philippines: 50M+ real-time transactions monthly via InstaPay

Cambodia: Bakong system facilitating $10B+ in digital transactions annually

Strategic Market Opportunities

Some markets are already shaping up as strong contenders for B2B payment innovation:

What Might Implementation Look Like?

For anyone trying to understand how this opportunity could be unlocked, here are a few themes worth tracking:

✅ Solution-Centric Design

Embed payments into ERP and supply chain platforms

Automate reconciliation and reduce manual processes

Integrate liquidity management features alongside payments

✅ Regulatory Alignment

Partner with central banks on infrastructure initiatives

Align solutions with national priorities (e.g., India’s MSME push)

Test innovations in regulatory sandboxes

✅ Value-Added Services

Embed working capital and credit tools into payment platforms

Use data analytics to optimize cash flow and supplier payments

Offer ESG-compliant tracking and reporting features

Final Thoughts: The providers that will lead this space won’t just process payments—they’ll build comprehensive financial operating systems for businesses, tailored to APAC’s unique challenges and opportunities.

I’m still learning and exploring this landscape, and I’d love to hear from others who are too. What are you seeing in the world of enterprise payments across APAC?

Private label cards are no longer confined to traditional closed-loop systems. By leveraging existing scheme rails, they significantly reduce the cost of implementation while maintaining the advantages of retailer-controlled payment solutions. This shift enables retailers to sidestep legacy closed-loop infrastructure, making private label cards more scalable and accessible. As a result, they are directly challenging traditional closed-loop providers and redefining how merchants engage with customers through proprietary payment solutions.

How Private Label Cards Work: A Deep Dive into Their Growing Popularity

In today’s competitive retail and e-commerce landscape, businesses are continuously seeking innovative ways to drive customer loyalty and boost revenue. One such tool that has gained significant traction is the private label card. These cards, often issued by retailers, offer customers exclusive benefits while providing businesses with greater control over their payment ecosystem. But how exactly do private label cards work, and why are they becoming increasingly popular?

What is a Private Label Card?

A private label card is a store-branded credit card that can only be used within a specific retailer’s network. Unlike traditional credit cards that operate on open-loop networks such as Visa, Mastercard, or Amex, private label cards function on a closed-loop system, meaning transactions are restricted to a particular brand or group of affiliated merchants.

These cards can come in different forms:

Charge Cards – Requiring full payment at the end of each billing cycle.

Revolving Credit Cards – Allowing customers to carry a balance and pay interest over time.

Prepaid or Stored Value Cards – Preloaded with funds that can be used until depleted.

How Do Private Label Cards Work?

Issuance – Retailers typically partner with financial institutions or fintech providers to issue private label cards. Some large merchants may also run their own card programs through in-house financing.

Customer Enrollment – Shoppers can apply for the card at the point of sale, online, or via mobile apps, often with minimal approval requirements compared to general-purpose credit cards.

Usage & Benefits – Once approved, cardholders can use their private label cards exclusively at the retailer’s stores (physical or digital) to make purchases and enjoy benefits such as discounts, rewards, or deferred payment options.

Billing & Payments – The retailer or financial partner manages the billing, collects payments, and may charge interest on revolving balances.

Data Insights & Customer Engagement – Retailers gain valuable transaction data that helps them tailor promotions, refine loyalty programs, and drive repeat purchases.

Why Are Private Label Cards Gaining Popularity?

Stronger Customer Loyalty – By offering special financing options, rewards, and discounts, businesses can encourage repeat purchases and deeper engagement.

Higher Spend per Customer – Studies show that customers using private label cards tend to spend more than those using regular credit or debit cards.

Better Margins for Retailers – Since private label cards operate without traditional card network fees, merchants save on interchange costs while also earning interest revenue from credit balances.

Enhanced Customer Insights – Unlike traditional bank-issued cards, retailers get full access to customer purchasing behaviors, allowing them to craft personalized offers.

Alternative to Traditional Credit – Private label cards often have more flexible approval criteria, making them accessible to a broader range of consumers, including those with limited credit history.

Disrupting Traditional Closed-Loop Providers – Private label cards are now leveraging existing scheme rails, reducing the cost of implementation and making them more scalable compared to traditional closed-loop card providers. This shift enables retailers to sidestep legacy closed-loop infrastructure while still maintaining brand control and customer engagement, effectively challenging traditional closed-loop providers in the market.

Key Players in the Private Label Card Space (APAC Region)

Several key players in the Asia-Pacific region are driving the adoption of private label cards:

AEON Credit Service (Japan, Malaysia, Hong Kong, Thailand, and Indonesia) – Offers private label and co-branded credit cards, focusing on retail, consumer finance, and installment plans.

HDFC Bank (India) – Partners with leading retail brands to offer store-branded private label credit cards with loyalty benefits.

Bank Central Asia (BCA) (Indonesia) – Provides private label and installment-based card solutions for local retailers.

UnionPay (China & Southeast Asia) – Supports private label card issuance in partnership with domestic banks and retailers.

CIMB Bank (Malaysia, Singapore, Thailand, Indonesia, and the Philippines) – Works with retailers to develop private label financing and payment solutions.

JCB (Japan & APAC markets) – A dominant payment network that enables private label solutions for regional merchants.

Challenges & Considerations

While private label cards offer numerous benefits, retailers must also consider:

Credit Risk – Managing delinquencies and defaults can be challenging if customers fail to repay their balances.

Limited Acceptance – Since these cards are restricted to specific merchants, they may not be as appealing as general-purpose credit cards.

Regulatory Compliance – Financial institutions and retailers must adhere to local lending and data privacy laws when operating private label programs.

The Future of Private Label Cards

As embedded finance and loyalty-driven payments evolve, private label cards are likely to become even more sophisticated. Innovations such as Buy Now, Pay Later (BNPL) integrations, digital wallets, and AI-driven personalized offers will further enhance their appeal. For businesses looking to deepen customer relationships while maintaining control over their payment flows, private label cards remain a powerful tool.

The B2B payments market in APAC is set to exceed $1.1 trillion by 2025, yet FMCG and Agri-Chemical companies still struggle with fragmented supply chains, disconnected ERP systems, and manual payment flows. The result? Lost sales, inefficiencies, and untapped revenue opportunities for manufacturers, distributors, and retailers alike.

The Gaps: Why Traditional Systems Are Holding FMCG Back

📌 Data Reconciliation Issues – Purchase order mismatches, pricing discrepancies, and disputes over defective items create friction between FMCG companies and their B2B buyers.

📌 Lack of Real-Time Sales & Inventory Visibility – FMCG brands rely on outdated sales data, making inventory planning and restocking inefficient.

📌 Manual Promotion Execution – Promo tracking is still done manually (e.g., wrapping shampoo bottles together for a combo offer), limiting real-time insights and effectiveness.

📌 Cross-Border & FX Inefficiencies – Many FMCG companies operate across Indonesia, Vietnam, the Philippines, and Malaysia, but FX volatility and high remittance costs slow down payments and impact working capital.

The Solution: A Closed-Loop, Data-Driven B2B Payment Ecosystem

To bridge these gaps, FMCG and Agri-Chemical firms must go beyond ERP-driven operations and leverage fintech-enabled B2B payments and embedded finance solutions.

Imagine a unified payments and data platform that:

✅ Integrates FMCG & B2B Buyer ERPs – Creates a real-time visibility layer between manufacturers, distributors, and retailers.

✅ Automates SKU-Based Promotions at POS – Instantly validates discounts, applies offers, and ensures compliance without manual intervention.

✅ Embeds A2A & Card-Based Payments – Leverages virtual cards, QR payments, and commercial payment railsto optimise cash flow and working capital.

✅ Enhances Supply Chain Finance – Provides instant, data-driven financing options for B2B buyers using transaction-level insights.

✅ Supports FX & Cross-Border Payments – Streamlines remittances, reducing settlement delays and costs for FMCG operating across Southeast Asia.

How Networks & Fintech Players Are Already Driving This Shift

Qwikcilver / Pine Labs has already built powerful closed-loop solutions:

✔ Automated SKU-Based Promotions – Plugging loyalty solutions into payment terminals to offer instant discounts at checkout.

✔ High Volume Transactions – With over USD 3 billion in annual sales processed through its platform, Qwikcilver serves more than 500 large retailers and brands across the APAC region.

✔ Customised Loyalty Solutions – From Visa and Mastercard prepaid solutions to multi-partner loyalty programs, Qwikcilver enables FMCG companies to create tailored experiences for their distributors and consumers.

✔ Enhanced Transparency and Real-Time Reporting – A central hub for distributor sales, product promotions, and inventory optimisation, which helps FMCG firms track everything from sales rep performance to outlet promotions.

Mastercard is already moving towards modernising B2B payments:

🚀 Mastercard Track & Commercial Cards – Expanding acceptance of virtual cards for B2B procurement & cross-border trade.

🚀 Collaboration with Boost (Malaysia) – Helping FMCG players digitalise last-mile distribution via embedded fintech.

🚀 Consumer Goods Team Initiative – Dedicated support for sales, finance, and supply chain optimisation.

Visa has also been a key player in enhancing B2B payments in this space:

🚀 Visa B2B Connect – A cross-border payments platform built to streamline and speed up transactions between large corporate buyers and suppliers in Southeast Asia, including FMCG brands.

🚀 Visa’s Commercial Payment Solutions – Facilitating digital B2B payments through virtual cards and digital wallets, enabling FMCG firms to optimize working capital and make better purchasing decisions in real time.

🚀 Collaboration with Payoneer – Visa’s partnership with Payoneer supports cross-border payments and streamlines transactions for FMCG and Agri-Chemical companies, simplifying FX and reducing manual efforts.

The Future: FMCG & B2B Payments Networks Must Evolve Together

The opportunity for Mastercard, Visa, and fintech players is clear: B2B payments need to move beyond transactions and become enablers of sales growth, inventory efficiency, and loyalty engagement.

The question is: Who will lead this transformation in APAC? Would love to hear thoughts from industry leaders driving B2B & FMCG payment innovation!

Small and medium enterprises (SMEs) form the backbone of Southeast Asia’s economy, contributing over 40% of GDPand accounting for more than 70% of employment in countries like Indonesia, Malaysia, the Philippines, Thailand, and Vietnam. Yet, despite their economic significance, many SMEs have historically relied on cash transactions, limiting their ability to access credit, automate operations, and scale efficiently.

The rapid adoption of digital wallets, projected to facilitate transactions worth $320 billion in Southeast Asia by 2025(Google, Temasek & Bain e-Conomy SEA report), is transforming this landscape. Wallets are not just enabling digital payments—they are serving as a launchpad for SME growth, offering financial access, automation, and enhanced customer engagement.

The Wallet Revolution in Southeast Asia

Digital wallets have gained significant traction due to high smartphone penetration, increasing digital literacy, and government-led financial inclusion initiatives. Players such as GrabPay, GoPay, OVO, ShopeePay, MoMo, TrueMoney, and GCash have seen widespread adoption, with Southeast Asia now home to over 500 million digital wallet users(Bain & Co, 2023).

For SMEs, the impact of wallets extends beyond convenience, driving meaningful improvements in financial access, transaction efficiency, and business automation.

1. Unlocking Financial Access for SMEs

Lack of access to formal credit remains a major hurdle for SMEs, with 51% of micro and small enterprises in the region unable to secure traditional bank loans (World Bank). Digital wallets are addressing this gap by:

Leveraging transaction data for alternative credit scoring, allowing previously unbanked SMEs to access microloans and BNPL financing.

Enabling embedded finance solutions, such as working capital loans and revenue-based financing, directly within wallet ecosystems.

Partnering with financial institutions to offer instant credit lines, helping businesses manage cash flow challenges.

For instance, GCash in the Philippines has launched GCredit, a lending feature that has disbursed over ₱50 billion (nearly $900 million) in loans to SMEs and individuals who previously lacked access to traditional banking services.

2. Enabling Faster and More Efficient Transactions

In a region where cash still accounts for over 50% of transactions (Visa Consumer Payment Attitudes Study, 2023), digital wallets are helping SMEs shift to cashless payments. QR code-based payments have:

Reduced checkout times by 40%, improving customer experience.

Lowered operational costs by eliminating cash-handling risks and reconciliation errors.

Indonesia’s QRIS (Quick Response Code Indonesian Standard), which allows interoperability between multiple wallets and banks, has facilitated over $15 billion in transactions as of 2023, benefiting SMEs by simplifying digital payment acceptance.

3. Integrating with Business and Loyalty Tools

Modern wallets are evolving into business enablement platforms, offering SMEs access to:

Loyalty and rewards programs, helping businesses increase repeat transactions by up to 25% (McKinsey, 2023).

Automated invoicing and settlements, reducing human errors and administrative workload.

E-commerce integrations, allowing businesses to accept seamless in-app payments on platforms like Shopee and Lazada.

A great example is ShopeePay, which provides instant cashback campaigns and in-app merchant promotions that drive both sales and brand loyalty for SMEs.

4. Driving Operational Automation

Many digital wallets now include built-in automation tools that help SMEs streamline operations:

Payroll disbursement tools, reducing manual payout times by 60%.

Supplier payment automation, ensuring on-time settlements with minimal intervention.

AI-powered financial insights, helping SMEs optimize expenses and inventory.

For instance, GrabPay’s merchant dashboard allows businesses to track sales trends, monitor cash flow, and manage multiple revenue streams—all within a single platform.

5. Expanding Market Reach

Cross-border e-commerce in Southeast Asia is growing at 30% YoY (Google, Temasek & Bain, 2023), and wallets are playing a crucial role in enabling SMEs to:

Accept payments from international customers without the complexities of FX conversion.

Leverage super apps (e.g., Grab, GoTo) to list products and reach millions of users within an integrated ecosystem.

Tap into government-backed digitalization programs that encourage cross-border trade.

Thailand’s PromptPay and Singapore’s PayNow, which recently integrated, allow SMEs to transact seamlessly across borders, reducing remittance costs and increasing transaction speed.

The Future of Wallets and SME Growth in Southeast Asia

As digital wallets continue to evolve, we can expect advancements in:

Embedded finance: More sophisticated credit models and SME insurance products.

AI-driven analytics: Predictive insights for personalized financing and marketing.

Blockchain-powered security: Enhancing fraud prevention and transaction transparency.

Governments and fintech players must collaborate to extend wallet adoption to underserved rural areas, ensuring financial inclusion at scale. The Philippines, Indonesia, and Vietnam still have over 50 million unbanked SMEs, representing a massive opportunity for wallet-driven solutions.

A Special Focus on Taiwan

While my work has primarily focused on the Southeast Asian fintech landscape, Taiwan holds a special place in my heart due to my family connections and deep affinity for the market. Taiwan’s digital economy has been growing rapidly, and its SMEs are undergoing a similar transformation as those in Southeast Asia.

Taiwan is home to over 1.5 million SMEs, which account for 98% of all businesses and contribute significantly to employment. The government has actively promoted digitalization, with initiatives like the Digital Transformation Plan for SMEs and the “Taiwan Pay” ecosystem, fostering greater adoption of e-payments.

Unlike some Southeast Asian markets, where digital wallets are primarily driven by super apps, Taiwan’s digital wallet landscape is more diversified, with key players like JKOPay, LINE Pay, and PX Pay leading the market. As of 2023, Taiwan’s mobile payments penetration rate reached nearly 60%, showing strong adoption among both consumers and businesses.

For SMEs in Taiwan, digital wallets offer key advantages:

Faster access to credit: Platforms like JKOPay offer microloans and BNPL solutions to help SMEs manage cash flow.

Integration with supply chain financing: Helping merchants streamline B2B transactions.

Government-backed digital incentives: Programs such as Triple Stimulus Vouchers, which encouraged digital spending, played a major role in shifting consumer behavior toward e-wallets.

Given my personal connection to Taiwan, I see a tremendous opportunity for digital wallets to further accelerate SME digitalization, particularly in cross-border e-commerce, as Taiwan-based businesses increasingly engage with Southeast Asian markets.

Summary:

The digital wallet revolution in Southeast Asia and Taiwan is not just about payments—it’s about enabling SMEs to automate operations, access credit, and expand their market reach. The intersection of wallets, AI, and embedded finance will define the next phase of SME digitalization, creating a more inclusive, efficient, and growth-orientedfinancial ecosystem.

Given my deep professional and personal interest in these markets, I am keen to see how digital wallets will continue to evolve and shape the future of SMEs.